Four themes to watch as earnings season shifts into focus

Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways:

- Ten out of 11 sectors are set to post positive earnings per share growth this earnings season

- Despite periodic negative headlines, AI capex is showing no signs of a slowdown

- With earnings expectations already at lofty levels, guidance will be key

Despite geopolitical headwinds, the broader macro backdrop remained constructive in the first half of the year. Economic growth proved resilient, consumers kept spending and the S&P 500 gained 10%. That favorable mix drove strong earnings growth, with S&P 500 earnings rising 27% year over year in 1Q26, led by the tech sector.

With 2Q26 earnings season set to ramp up next week, investor focus will increasingly shift from the macro environment to company execution, as results and management commentary take center stage. Consistent with our 12-month price target of 8,200, we expect another quarter of robust (+22%) earnings growth, driven largely by the ongoing AI infrastructure buildout. However, expectations have climbed alongside the equity market’s rally, raising the hurdle for companies to exceed already lofty consensus forecasts.

Below, we highlight four key issues we'll be monitoring in the weeks ahead:

Is equity market broadening backed by fundamentals?

Equity market broadening has been a defining theme this year. For the first time since 2022, the equal-weighted S&P 500 is outpacing the market-cap weighted index (by +1.3%). Meanwhile, small caps have outperformed large caps by 10% – the widest margin since 2003. Importantly, earnings growth is beginning to broaden. While much of this bull market’s earnings growth has been concentrated in tech, consensus estimates point to 10 of the S&P 500’s 11 sectors – all except health care – posting positive earnings per share (EPS) growth in 2Q26. S&P 500 ex-MAGMAN* earnings are projected to grow ~17%, the fastest pace since 4Q21. Broader participation suggests the market is becoming less reliant on a narrow group of leaders, supporting a continuation of the bull run.

Can AI continue to propel tech earnings?

During the lull between earnings seasons, the tech sector came under pressure amid concerns over reports of companies scaling back AI-related spending. As a result, the tech sector remains 7% off its recent 52-week high – the fourth-steepest decline among sectors, behind energy, communications services and consumer staples.

This earnings season, investor attention will shift back to company-reported results – rather than anecdotal headlines – likely providing renewed support for the sector. Consensus expects tech earnings to grow 62% year over year, surpassing 1Q26’s already impressive 53%. While 2Q likely marks the high point of the EPS growth rate, that does not imply peak earnings. Tech earnings are expected to grow more than 20% every quarter through 2027, supporting our overweight stance.

Despite concerns that hyperscalers may start to moderate AI-related capital spending, we expect capex plans to be reaffirmed and to rise through 2028. Why? Because there is tangible evidence that businesses benefit from AI adoption. Mentions of AI across all 11 sectors are up 98% year over year, reaching new highs.

The average net margin for the equal-weighted S&P 500 could set a record in 2Q – reflecting, among other factors, AI’s benefits for corporate profitability. As the capex cycle continues, it’s also important to note that hyperscalers in aggregate may return to positive free cash flow by 2028, thereby addressing investor concerns about balance sheet risk.

Are consumer fundamentals poised to improve in the second half of 2026?

Real-time economic indicators continue to point to a healthy consumer. Redbook sales – a measure of department store spending – are growing at their fastest pace since 2022, airline traffic remains positive year over year and restaurant bookings are still running more than 10% above year-ago levels.

That said, consumer headwinds mounted during 2Q as higher fuel prices and broader inflationary pressures diminished purchasing power. Real wage growth fell for two consecutive months for the first time since 2022, while the savings rate dropped to a four-year low. These headwinds have weighed on consumer discretionary stocks – the only sector in negative territory year to date – and this sector’s 2Q earnings (ex-Amazon) could decline ~5% year over year.

Looking into the second half of the year, a broadly healthy labor market and cooling fuel prices should support a more constructive consumer outlook. While selectivity remains important, bearing in mind that consumer spending is heavily driven by upper-income cohorts, positive management commentary could provide a catalyst for a sector that has lagged in recent months.

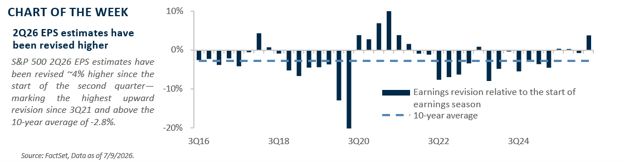

Can corporate guidance top already lofty expectations?

The S&P 500’s ~10% gain year to date has been supported by fundamentals: Robust earnings growth has helped to moderate P/E ratio multiples even as the market has moved higher. However, expectations are elevated ahead of earnings season.

Second-quarter EPS estimates have been revised 3.8% higher since the start of the quarter – the largest increase since 3Q21 – while full-year 2026 and 2027 EPS estimates have risen nearly 10% year to date, among the strongest upward revisions since 2000. This lofty bar heightens the potential for earnings-related volatility, particularly for companies that miss estimates or disappoint on guidance, as recent pullbacks in several early reporters (e.g., PepsiCo and Korea-based Samsung) have demonstrated.

Here is the big picture: With the economy on solid footing and AI continuing to drive capex, we believe much of the recent upward revisions are justified. Our year-end and 12-month S&P 500 targets of 7,650 and 8,200, respectively, reflect EPS of $326 in 2026 (~20% growth verus 2025) and $352 in 2027. This reinforces our view that earnings – rather than multiple expansion – will remain the primary driver of returns for the foreseeable future.

*MAGMAN represents a composite of Microsoft, Apple, Google, Meta, Amazon, Nvidia. The foregoing is not a recommendation to buy or sell MAGMAN stocks.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.